Economy and demographics

Dutch economy shrugs off potential impact of Brexit vote

Despite the initial fears triggered by the Brexit vote, the Dutch economy continued its steady recovery in 2016 and economic growth of over 2% actually outpaced earlier projections. This economic growth was driven by rising business confidence and the resultant rise in business investments, on the back of a steady rise in manufacturing output and continuing export growth. The main negative uncertainties relate to events outside the Netherlands. The uncertainty triggered by the Brexit vote and the recent U.S. elections, plus a potential economic slowdown in China, may put a damper on growth and confidence, while geopolitical tensions in various parts of the world continue to pose a risk to the global economy.

Population growth continues

Recent decades have seen strong population growth and it is expected to continue in the coming years. The total population and the number of households are expected to continue growing until 2040, stimulating overall consumer spending. The current population is expected to increase from 16.9 to 17.6 million by 2025, while the number of households is set to rise by 70,000 each year from the current 7.7 million to 8.3 million by 2025 and 8.6 million by 2040.The largest growth is set to be in single-person households, which are expected to increase from 2.9 million to 3.3 million by 2025.

Trends and developments in the hotel market

Strong tourism demand with limited growth of supply

Hotel operators remain positive, as tourism in the Netherlands continues to grow. UNWTO reported an increase of 7.0% in Dutch tourism in 2015. For 2016, UNWTO has calculated an increase of around 1.2 million tourists (8,0%) to 15.5 million. Amsterdam in particular benefited from the increase in foreign tourist arrivals and remains the most popular tourist destination in the Netherlands. The depreciation of the euro also helped to push tourism. In reaction to the strong tourism demand, the Dutch hotel market has increased in size significantly in recent years. The Dutch star-rated hotel market consists of approximately 2,160 hotels and more than 100,700 rooms, with 30,000 of these rooms in Amsterdam. The number of homes offered through Airbnb in Amsterdam remained stable around a total figure of 14,000 rooms or homes. However, Amsterdam city council is trying to gain greater control in this far from transparent sub-segment. Thanks to the rapid pace of hotel development in Amsterdam, the city is already set to add approximately 6,500 rooms to its current stock. Restrictive hotel development policies will limit the development of new hotels, which should be favourable for existing stock after 2020, when the majority of new supply will have been added to the total stock. The Hague and Eindhoven might provide interesting opportunities, due to the limitations on planned future hotel supply.

Market fundamentals on the up

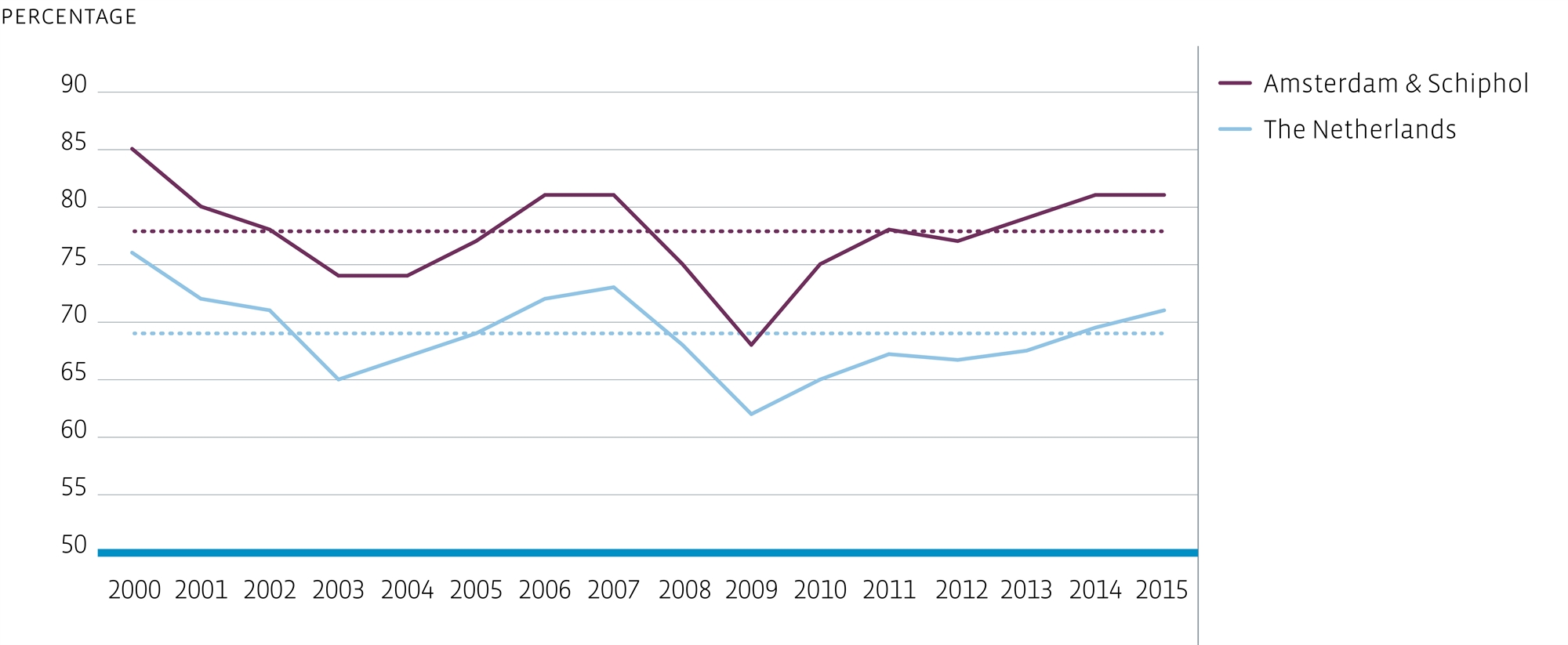

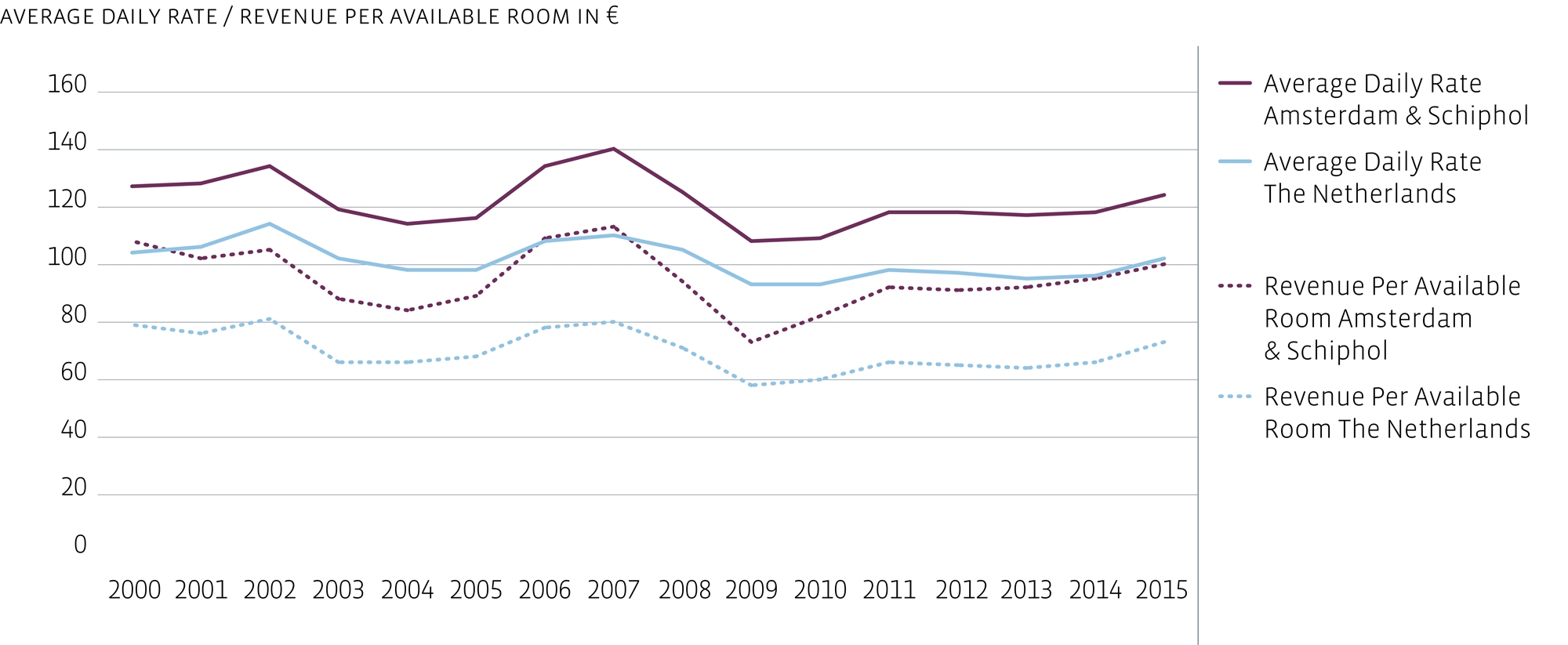

Data from Horwath shows that occupancy and room rates, and thus the RevPAR (Revenu Per Available Room), of Dutch hotels increased in 2016. Overall occupancy levels in the Netherlands stood at around 71% and average room rates have increased to €101 per night last year. In Amsterdam occupancy rates increased by 0.2% to a level of 81% in 2016. The RevPAR growth in Amsterdam for 2016 and 2017 are expected to be 2.5% and 2.1% respectively. With a daily rate of € 135, Amsterdam hotel rooms stand out in comparison to other regions of the Netherlands. Despite the strong rise of Airbnb, hoteliers remain optimistic and expect occupancy rates and average room rates to rise in the next few years.

Dutch occupancy level

Risk free return, yields and yield gap

Airbnb affecting small traditional tourist hotels in lower segments

The number of homes and nights booked through Airbnb has increased significantly in recent years. The majority of these rooms are located in Amsterdam. With more than 80 percent of the total stock consisting of homes and apartments, and with average room rates above €143 per night, Airbnb targets tourist groups that are looking for a local sleeping experience. Primarily smaller traditional tourist-focused hotels with three stars or less are expected to continue to see competition from Airbnb. Hotels in higher segments or with a unique concept are better equipped to deal with the Airbnb phenomenon. Their sophisticated booking systems and intelligent sales and marketing programmes help them to secure healthy occupancy levels. Some of the large hoteliers are even trying to find ways to cooperate with Airbnb.

New leasehold conditions Amsterdam

Currently the municipality of Amsterdam is in a process of renewing the current leasehold conditions. Concept lease hold conditions have been published, which has led to quite some response and turmoil. The reaction of the municipality on this turmoil was that the municipality will review and analyse all reactions and that this may lead to an adjusted concept. At this moment it’s unclear what the final version of the lease hold conditions will encompass and if and to what extent these possibly adjusted lease hold conditions will affect the value of the investments of the Fund in Amsterdam. The Fund has over € 125 million exposure at year-end 2016 in Amsterdam for in total 3 properties. Bouwinvest is monitoring this matter closely and possible steps to mitigate any loss of investment values will depend on the outcome of the new leasehold conditions.

Implications for hotel real estate

Strong demand for Dutch real estate investments

After climbing to their highest level since 2007 in 2015, Dutch real estate investment volumes came in at € 13.5 billion in 2016, which is about 9% higher than the level in 2015. Of this figure, about € 355 million was invested in hotel real estate, which is roughly 2% higher than the total hotel investments in 2015. Foreign investors now account for around 55% of the total real estate investment volume and are showing continued interest in the investment market. With interest rates in the U.S. slowly increasing and real estate prices in other key markets such as London, Paris and Munich having already increased, investment momentum is picking up in continental Europe, including the Dutch real estate markets. More risk-seeking investors have become more active on both the buy and sell side. Supported by the economic recovery across the country, prices of secondary locations are expected to increase. However, the continuing interest of both Dutch and international investors is quickly pushing up prices. This trend is expected to continue in the coming years. For core investors, it is now essential to have the right relationships in the market and to be a partner in the early stages of development or buying processes, as this enables them to select the right assets for an attractive risk-return profile. Compared to more opportune competitors, investors with in-depth real estate knowledge and active asset management teams will be the ones that can add value and that will therefore outperform in the long run.

Amsterdam remains focus of investors

The total invested volume in Dutch hotels in 2016 amounted to €355 million. Amsterdam remains the major focus for investors. However, prime stock is becoming more scarce due to the restrictive hotel policy. As a result investors are pushed to the fringes of Amsterdam for new opportunities or take more risk by focusing on new concepts in the extended stay and budget segment, or taking up a certain amount of lease risk.

Investors risk appetite increases

The long-term average total return for pan-European Hotels sits well above the 7% level and has generally been more stable than for other real estate sectors. Yields across Europe remained stable in 2016, with prime yields in Amsterdam just below the 5.5% level. With interest rates at a historically low level, the average yield gap for Amsterdam hotels stands at a high level of 400 bps, beating almost all core markets in Western Europe. The majority of investors expect yields to shift downwards as the search for yield continues.

Inner city, well positioned hotels, combining tourist and business travellers will outperform

Increasing supply levels in combination with modest domestic demand expectations for the near term will create a challenging environment. Well positioned inner city hotels offering fresh and innovative concepts are set to outperform. Hotel formats that are able to attract tourists and business travellers have the highest chance of outperformance. These hotels are best equipped to cope with trends like Airbnb, which mainly affects tourist demand, and are less dependent on business demand which correlates strongly with the economic environment. Again, the Amsterdam market is the best placed, enjoying as it does a balanced mix of business and leisure visitors. However, the restrictive hotel policy in Amsterdam requires new hotel initiatives to offer a unique concept and provide additional value to the locality, which is resulting in new concepts. In 2016, a total of 15 hotels opened in the city, adding some 2,100 rooms to the total stock. The capital is set to add around 1,970 new hotel rooms in the period 2017-2018.