Economy and demographics

Dutch economy shrugs off potential impact of Brexit vote

Despite the initial fears triggered by the Brexit vote, the Dutch economy continued its steady recovery in 2016 and economic growth with al level above 2% actually outpaced earlier projections. This economic growth was driven by rising business confidence and as a consequence a rise in business investments, on the back of a steady rise in manufacturing output and continuing export growth. The main negative uncertainties relate to events outside the Netherlands. The uncertainty triggered by the Brexit vote and the recent U.S. elections, plus a potential economic slowdown in China, may put a damper on growth and confidence, while geopolitical tensions in various parts of the world continue to pose a risk to the global economy.

Population growth continues

Recent decades have seen strong population growth and it is expected to continue in the coming years. The total population and the number of households are expected to continue growing until 2040, stimulating overall consumer spending. The current population is expected to increase from 16.9 to 17.6 million by 2025, while the number of households is set to rise by 70,000 each year from the current 7.7 million to 8.3 million by 2025 and 8.6 million by 2040.The largest growth is set to be in single-person households, which are expected to increase from 2.9 million to 3.3 million by 2025. In addition, the number of people older than 75 years is expected to double over the next 25 years. As a result, the work population will show virtually no growth over the coming years.

Quantitative gap – Urbanisation

The Dutch market is characterised by marked regional differences in housing demand, with the heaviest demand concentrated in regions with a healthy economic and demographic outlook. Population growth and the increase in the number of households is expected to be well above the national average in certain ‘core’ regions, such as the Randstad urban conurbation (Amsterdam, Utrecht, Haarlem, Rotterdam and The Hague) and the Brabantstad conurbation (Breda, Eindhoven, Helmond, Den Bosch and Tilburg). However, population is expected to fall in some peripheral regions in the north and east of the country. Both urbanisation and ageing will lead to transformation in the real estate market for all real estate sectors in the next few decades.

Trends and developments in the healthcare market

Ageing population

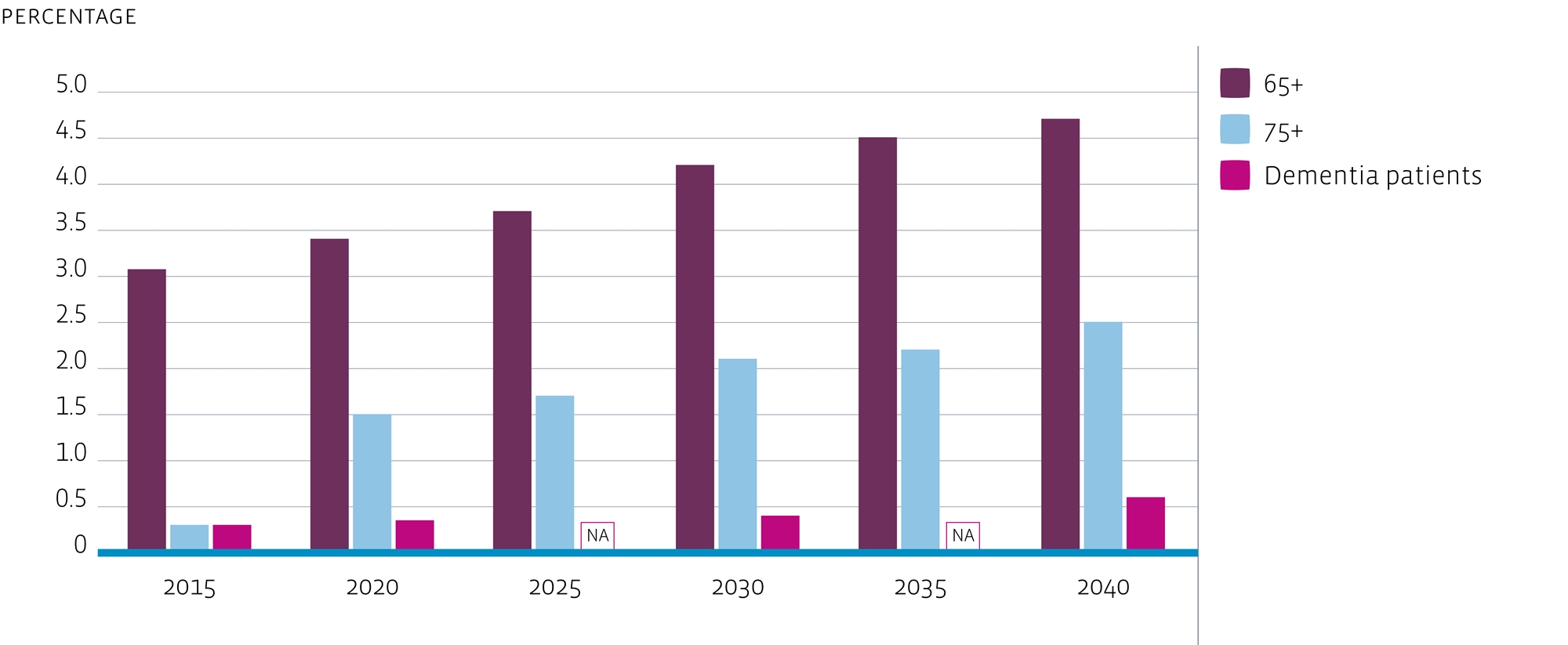

Another trend that is changing housing demand is the ageing population. Between 2016 and 2030 the number of elderly is forecast to grow by some 875,000 households, an increase of 44%. Many retirees, especially those living in the larger cities, are expected to sell off their existing properties and rent smaller, higher-quality and low-maintenance homes. These so called 'assisted living' dwellings provide a combination of housing and care 'at arm's length', with 'care proof' floor plans, the possibility to arrange 24x7 care, and a certain social context (as loneliness is a serieus issue for the elderly).

However, ageing is not the only driver for healthcare investment. Unlike the expected ‘double greying’ of the elderly population (there will be more older people, who will also be increasingly older), the need for care for people with a mental or physical disability is expected to grow less than the general population. The current size of the disabled population that cannot live independently is approximately 75,000 people, of 9% has a physical disability. This group is expected to remain stable with respect to size.

These developments lead to the following forecasts with respect to the growing target groups for healthcare real estate investments:

65-plus to 26% from 16%;

80-plus to 9% from 4%;

Dementia: will affect 538,000 people compared with 264,000 people today;

Disabled market stable at around 75,000 people requiring serious care

Increase of elderly and dementia patients

Qualitative mismatch – Single-person households are changing the market

In addition to the quantitative shortage, the qualitative gap between housing supply and demand is also set to widen, due in part to the increasing number of smaller households and – forecasts are predicting that the G4 cities will see 20% to 40% more single-person households over the next 15 years, with an average expectation of 28%. For Amsterdam, this implies an increase of over 70,000 single-person households. On a national level, the number of single-person households is set to grow by approximately 600,000.

Qualitative catch-up – Investments needed for future-proof real estate

Despite the fact that budget cuts have limited investments in recent years, many institutions are now anticipating future growth. Apart from increasing demand for care services and real estate, the sector (both care for the elderly and the mentally disabled) also faces a qualitative mismatch, as many of their current buildings are fairly out-dated. In order to make the healthcare sector future-proof, a catch-up in quality is needed in the years ahead. In order to achieve this, organisations are more and more focusing on their core business, that is delivering high quality care, in stead of operating and maintaining real estate.

Increasing diversity in the market

The fact that a large group of clients is now responsible for their own accommodation means that they have the freedom to live wherever they want – these clients receive care services at home. This freedom of choice is having a major impact on the market and we expect to see the emergence of a more diversified market. For example, people with higher living standards are expected to demand the same quality when they need care services. Also, people are expected to give location more weight in the choices they make.

Housing associations step away from the market

In the past, housing associations rented out large amounts of real estate to Dutch healthcare institutions. Due to government reforms, housing associations are now limiting their healthcare real estate services and they are expected to withdraw from the market in phases. However, this is only possible if there are alternatives on the market. Institutional investors are expected to play their part in the near future.

New leasehold conditions Amsterdam

Currently the municipality of Amsterdam is in a process of renewing the current leasehold conditions. Concept lease hold conditions have been published, which has led to quite some response and turmoil. The reaction of the municipality on this turmoil was that the municipality will review and analyse all reactions and that this may lead to an adjusted concept. At this moment it’s unclear what the final version of the lease hold conditions will encompass and if and to what extent these possibly adjusted lease hold conditions will affect the value of the investments of the Fund in Amsterdam. The Fund has exposure at year-end 2016 in Amsterdam for one property. Bouwinvest is monitoring this matter closely and possible steps to mitigate any loss of investment values will depend on the outcome of the new leasehold conditions.

Implications for healthcare real estate investments

Strong demand for Dutch healthcare real estate investments

After climbing to their highest level since 2007 in 2015, Dutch real estate investment volumes came in at € 13.5 billion in 2016, which is about 9% higher than the level in 2015. Of this figure about € 237 million was invested in health care real estate. A small portion, however 76% higher than the total health care investments in 2015, which were € 135 million according to PropertyNL Research.

Foreign investors now account for around 55% of the total real estate investment volume and are showing continued interest in the investment market. With interest rates in the U.S. slowly increasing and real estate prices in other key markets such as London, Paris and Munich having already increased, investment momentum is picking up in continental Europe, including the Dutch real estate markets. More risk-seeking investors have become more active on both the buy and sell side. Supported by the economic recovery across the country, prices of secondary locations are expected to increase. However, the continuing interest of both Dutch and international investors is quickly pushing up prices. This trend is expected to continue in the coming years. For core investors, it is now essential to have the right relationships in the market and to be a partner in the early stages of development or buying processes, as this enables them to select the right assets for an attractive risk-return profile. Compared to more opportune competitors, investors with in-depth real estate knowledge and active asset management teams will be the ones that can add value and that will therefore outperform in the long run.

Liquidity rises in healthcare investment market

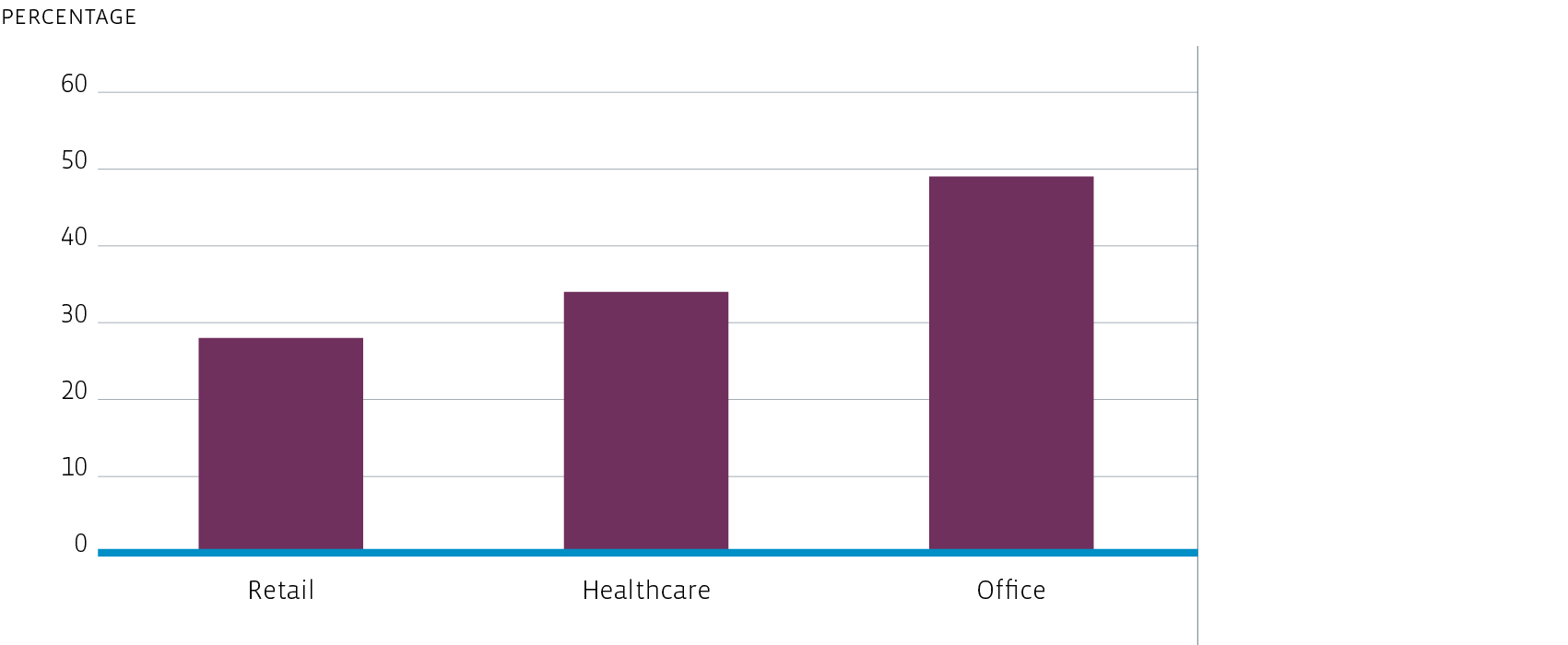

Investment and liquidity in the health care real estate investment market showed a big year-on-year increase in 2016. Last year saw an increase in the number of new investors. In case of a continuing trend, this means an increased competition for attractive investment properties and might result in some yield compression. However, this will also have a positive impact on portfolio valuations and boost indirect returns. The parts of the cure and care markets together that is interesting for institutional investors (between roughly 2,000 and 100,000 m²) currently occupy an amount of floor space somewhere between the retail market and the office market. Current estimates put this floor space at the same level of 34 million m² for the care segment alone by 2030.

Size of real estate markets in mln m² (source EIB)

Healthcare market as investment grade real estate

The Economic Institute for the construction industry (EIB) has defined a number of criteria an investment in healthcare real estate would have to meet to qualify as investment grade real estate:

The property is part of a market with a certain scale in which buildings have comparable features and comparable economic exposure (the same legislation and regulations). The property should also be distinctive when compared with other investments (in real estate).

A large (potential) market contributes to marketability, which means that real estate is more easily traded.

The property (or the portfolio of properties) should be of sufficient volume in itself to be an interesting investment for investors.

The housing regime must provide the freedom (both physical and policy-wise), to enable the reasonable commercial exploitation of the property and to be able to transform same if necessary.

The property should not be too large, as this would be too dominant (temporarily) from a portfolio point of view. Too large a property would also entail extra risks, for instance related to its potential transformation.

Limited government influence on the cash flow due to consistent policy, for instance due to a major share of self-financed payments by healthcare clients.

Finally, a solid tenant is required, both by private individuals and by care providers. This reduces the risk of vacancy, which in turn makes the real estate a more attractive investment.

The Fund adheres to these criteria with respect to the acquisitions that are made.