Portfolio characteristics

47 Dutch retail properties (€ 778 million; 209,979 m²)

Focus on Experience and Convenience

Continuously high occupancy rate

Continuous outperformance of IPD Property Index

High percentage of green energy labels (A, B or C label)

GRESB Green Star

Focus on Experience and Convenience

Virtually all of the portfolio’s assets qualify as high-quality retail facilities. In line with our strategic focus, the properties can be divided into two segments:

EXPERIENCE - High street retail in best shopping cities

The main focus of the Fund’s Experience portfolio is on individual high street shops or clusters of shops in prime shopping areas in major Dutch city centres. These city centres have retained their market share and will continue to do so in the future. The historical surroundings, the varied supply of retail formulas, plus restaurants, museums and other cultural and leisure facilities help keep these shopping areas attractive and popular. In short, they offer today’s consumers the experience and ‘fun factor’ they demand, as shopping has become part of a ‘total experience’ for many consumers. Very importantly, these shopping areas are widely seen as the most future-proof segment of the retail market, and we believe this will continue to drive demand for retail space from a wide range of national and international fashion and lifestyle retail brands.

For strategic asset management and acquisition purposes, Bouwinvest and its research department retail experts have developed a ranking tool for the top shopping cities and high streets in the Netherlands, based on criteria such as footfall, average rent per m², vacancy rate, the number of inhabitants and average income in specific catchment areas. This tool provides an overview of the most attractive cities and shopping streets in the Netherlands.

CONVENIENCE - Shopping centres and solitary supermarkets with strong catchment area

A healthy catchment area is the main factor in the success of any shopping centre or supermarket with a focus on daily shopping needs. The size – and health – of a catchment area can be affected by the regional economy, the local and regional demographic outlook and competing retail stock. A healthy regional economy guarantees employment and income growth, while demographic growth has a visible impact on a shopping centre’s potential market. On the other hand, new retail stock can lead to a reduction in a centre’s effective catchment area.

The Fund focuses on a number of additional factors that increase the level of convenience so prized by today’s consumers, an element that the Fund believes will become ever more important in the future. These additional criteria include easy accessibility, comfort parking, an effective tenant mix, plus the overall look and feel of the centre. Demographic changes in for instance average age - or household size needs to be actively addressed through continuously optimising the property and its tenant mix. One essential part of the retail mix is one or two clear, complementary and well positioned supermarket anchors, as these act as a major ‘pull’ factor for convenience shoppers. An effective retail mix, with various specialist stores is another factor that makes shopping centres attractive to consumers. Due to market changes and the ongoing growth of online sales, the number of non-food shops in these centres will decline even more in the near future. Therefore the Fund is also focused on actively revitalising its convenience centres though increasing the average share in m2 and its cash flow from supermarkets, shops in daily goods and deliveries and decreasing the number of non-core units.

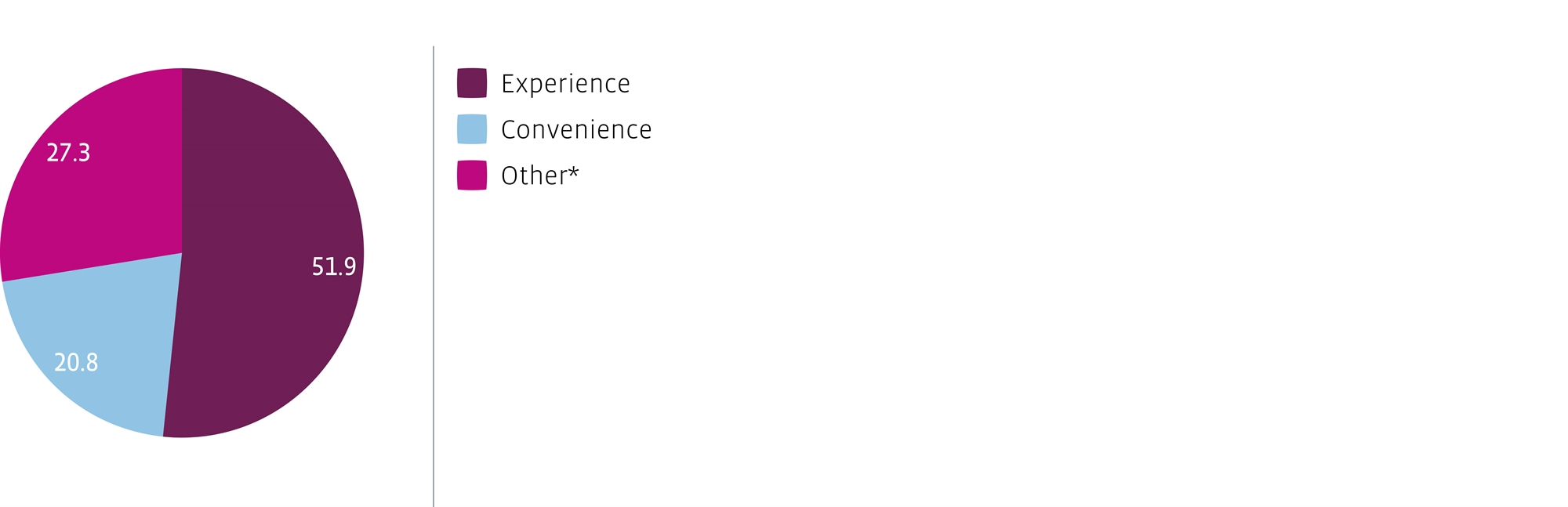

Portfolio composition by strategy as a percentage of market value

- *The category Other consists of retail assets that does not fully meet our strict Experience and Convenience criteria. The Fund aims to decrease

the share of Other in the existing portfolio to at least 20% of the portfolio value.