International investments

Bouwinvest's International Investments delivered a solid performance modest performance in 2016. The total return came in at 5.3%, excluding currency results and after management fees. In 2016, unlisted investments made the largest contribution to this result (7.7%). However, the return of the listed investments was negatively affected by the uncertainty in global markets and amounted to -3.5% (2015: 9.6%). Despite the growing competition, we were able to make new investments of EUR 279 million in 2016.

Unless stated otherwise, all returns mentioned below are excluding currency results.

Europe

Our European portfolio recorded a return of 2.7% in 2016, with returns pressured primarily by geo-political and macro-economic developments. These included the ECB’s continued loose monetary policy, immigration issues and of course the unexpected Brexit vote. On top of this, the UK increased stamp duty by 1%, which led to a corresponding drop in values. Our returns were also slightly negatively impacted by the sharp fluctuations in the GBP-EUR FX rate in EUR funds with exposure to sterling. However, the prevailing volatility in European markets – and elsewhere - did create some excellent opportunities to enter the market at the low end of the cycle. We made some very solid investments in commercial real estate (mainly offices and retail) in the Nordics, as well as gateway offices in main cities such as London, Paris, Berlin and Frankfurt, all of which have solid fundamentals. Lastly, we increased our listed investments in Western-European offices. A significant part of our UK exposure is in mezzanine finance, which offers protection from initial write-downs. Plus we have a lot of exposure to properties with very long leases. We expect these investments to continue to contribute to solid returns in the future.

North America

The US market was dominated by the presidential elections in 2016. Despite the uncertainty in the run-up to the election and the victory of Donald Trump, real estate fundamentals continued to improve last year, with rental growth above inflation and property yields still hovering around record lows, although at a comfortable cushion above US treasuries. The lower deferred tax liability as a result of the recent new FIRPTA regulations had a positive impact on the returns at total portfolio level and also improved the net return profile for value added strategies. The Northern American portfolio delivered another strong performance in 2016, ending the year with a total return of 8.8%. These results were bolstered by continued growth in demand and the lack of sufficient new supply. This led to rental growth in most US markets and sectors. There are concerns that the US market has peaked and we may see some cooling, but there will always be opportunities on a market this large. Prices are high at the moment, but these are largely justified by low interest rates and persistently strong investor demand. We continued to focus on the larger US cities last year, as these have the strongest fundamentals.

Asia-Pacific

The Asia-Pacific portfolio delivered a return of 2.7% in 2016. The region’s markets showed a certain level of volatility due to fears of an economic slowdown in China – which is still recording annual GDP growth of 6-7% – largely offset improving fundamentals in countries like Australia. Australian real estate funds with low leverage delivered solid double-digit growth. Japanese investments also performed well, but Singapore retail investments were hit by a weakening market. We also managed to sell office exposure at a good price. We expanded the Asia-Pacific portfolio last year, adding investments in the Pan-Asian hotel sector, which is growing rapidly thanks to the huge increase in tourist travel. We also invested in Australian student accommodation in a joint venture with Scape and APG. We are still very bullish on the Asia-Pacific region, and we made a number of top-up investments in Australian and Japanese real estate funds. Chinese economic growth is now much more sustainable than in the past and Australia, where we have a lot of investments, is proving remarkably resilient, with very strong fundamentals and a solid long-term outlook. The Bank of Japan’s buy-up of J-REITS is having a major positive impact on listed real estate investments in Japan and this is set to continue for some time.

Sustainability

Benchmark international real estate investments

Last year, Bouwinvest continued its active cooperation with other institutional investors aimed at increasing sustainability and transparency in the real estate sector. We extended our membership of GRESB as an investor member and encouraged the fund managers of our (international) indirect investments to participate in the GRESB benchmark and to improve their scores.

Highlights GRESB results international portfolio

Overall GRESB participation improved to 72% of bpfBOUW’s total international portfolio (2015: 65%);

69% of bpfBOUW’s international portfolio has a Green Star;

Index outperformance of bpfBOUW’s international portfolio with a score of 64 (compared with 60);

Energy consumption reduction of 4% and a 6% reduction in GHG emissions in bpfBOUW’s international portfolio in the period 2014-2015.

| | 2012 | 2013 | 2014 | 2015 | 2016 |

Response rate GRESB (based on NAV) | | | | | |

Listed | 82% | 76% | 55% | 62% | 58% |

Non-listed | 46% | 59% | 70% | 66% | 75% |

Total portfolio | 50% | 61% | 67% | 65% | 72% |

| | | | | | |

Outperforming benchmark GRESB listed | 79% | 75% | 78% | 83% | 94% |

Outperforming benchmark GRESB unlisted | 56% | 38% | 49% | 66% | 64% |

| | | | | | |

Number of Green Stars listed | 8 | 9 | 18 | 21 (out of 26) | 19 (out of 21) |

Number of Green Stars unlisted | 7 | 11 | 15 | 18 (out of 32) | 17 (out of 29) |

| | | | | | |

Listed improved performance (compared to last year) | n/a | 31% | 54% | 78% | 38% |

Unlisted improved performance (compared to last year) | n/a | 48% | 43% | 91% | 69% |

Dutch investments

Bouwinvest manages five Dutch investment funds, three of which are open to third-party investors. Our main focus is on the residential, office and retail sectors in what we have identified as our core regions. These regions all have an above–average economic and demographic outlook and will benefit from the above-mentioned megatrends, such as the urbanisation trend, the ageing of the population and the rise of new technologies. We also invest in the healthcare sector, as we believe the ageing of the population will continue to increase demand for real estate with a healthcare element. The rapid rise in tourism is also increasing demand for hotels. This is a positive development for our Hotel Fund.

Residential Fund

The Residential Fund generated a total return of 20.5% (2015: 12.5%), with a direct return of 3.4% (2015: 3.8%), and an indirect return of 17.1% (2015: 8.6%). The Fund had a high and stable average occupancy rate of 97.7%. Like-for-like rental growth for 2016 came in at 3.2% (2015: 3.8%), while rent arrears were low at 0.7% (2015: 0.9%). The dividend return for 2016 came in at 3.4% (2015: 3.8%).

The Residential Fund once again reaped the benefits of Bouwinvest’s growth strategy and its confidence in the residential market in recent years and saw the completion and delivery of eight excellent new-build projects, nearly all of which were fully let before completion. We currently have a secured pipeline of 11 new residential projects (1,063 apartments and 194 family homes) following investments of around € 255 million in 2016. Demand for high-quality homes the liberalised rental sector is still growing, especially in our core markets.

Thanks to the continued recovery in the residential sector and the very high quality of the residential portfolio, the Fund to attracted six new clients in 2016. This took the total number of clients to 16 as of January 2017.

At year-end 2016, the Fund’s property portfolio consisted of 237 properties with a total value of € 3.9 billion.

Retail Fund

The Retail Fund booked a return of 8.4 % in 2016 (2015: 4.5%), the result of a direct return of 4.6% (2015: 4.4%) and an indirect return of 3.9% (2015: 0.1%). The average occupancy rate was 94.7% (2015: 94.2%). The dividend return for 2015 was 4.6% (2015: 4.4%).

The Dutch economy continued to recover in 2016; this led to a strong rise in consumer confidence. Furthermore, international investors' boosted interest in retail real estate resulted in a yield shift. This in turn led to a healthy increase in the values of the Fund’s retail assets in Amsterdam and its other core regions in both the Experience and Convenience segments. The Fund continued to optimise its portfolio in 2016, adding new assets and redeveloping and upgrading existing assets. While retail real estate will remain a challenging sector in the years ahead, we believe that thanks to a good balance of 'Experience' and 'Convenience' oriented retail real estate assets, the Retail Fund’s portfolio will continue to generate solid returns in the years ahead.

In 2016, we saw the completion and delivery of the Nowadays redevelopment at Damrak/Nieuwendijk in Amsterdam, one of the largest retail redevelopments in the capital in decades. We also took delivery of the Stadionplein and Mosveld shopping centres in the Convenience segment. The Retail Fund invested around € 31 million last year and will continue to upgrade and future-proof existing assets and look for acquisitions that meet our quality and return requirements.

The Retail Fund attracted three new clients in 2016. As of 1 January 2017, we welcomed an additional new client, taking the total number of clients to five. We see this as an endorsement of our strategy of focusing on the experience and convenience segments of the retail market and a clear sign that investors still believe that the retail sector offers opportunities for stable long-term returns.

In 2016, the Retail Fund agreed new leases and renewed existing contracts for a total of 72,997 m² of space, representing a rental value of some € 16.6 million.

At the end of 2016, the Fund’s portfolio consisted of 47 properties with a total value of € 778 million.

Office Fund

The Office Fund booked a return of 5.5% in 2015 (2015: 0.5%), the result of a direct return of 3.6% (2015: 4.2%) and an indirect return of 1.9% (2015: -3.7%). The average occupancy rate was stable at around 81% in 2016 from 80.1% in 2015, largely due to the high proportion of properties we are currently redeveloping. The dividend return came in at 3.6% (2015: 4.2%). The strong turnaround in the indirect return was driven by higher valuations for a number office properties on the back of redevelopment plans.

After several years of outperformance as compared to the IPD index, the Fund’s relative performance dipped somewhat over the past two years. Last year was a year of portfolio optimisation for the Office Fund. The highlight of 2016 was the acquisition of the Hourglass, a mixed-use building in Amsterdam’s Zuidas business district. The Fund also invested € 3.0 million in the continued upgrade of the WTC Rotterdam and launched the redevelopment of the former Citroën buildings (The Olympic 1931 and The Olympic 1962) in Amsterdam.

In 2016, the WTC The Hague was awarded BREEAM-NL In-Use Excellent certification. This is the first time this score at building and building management level has been awarded to a multi-tenant asset in the Netherlands. Active asset management and continued investments in upgrading and updating its office assets ensured that the Fund renewed or signed new leases for a total of 15,509 m², representing an annual rental income of € 2.9 million in 2016.

The Fund attracted another new client in 2016, a clear demonstration of the renewed confidence in the office sector, as well as in the Office Fund’s strategy and the high quality of its portfolio. As of 1 January 2017, the Fund's total number of clients is three.

At year-end 2016, the Fund’s portfolio consisted of 16 properties with a total value of € 503 million.

Hotel Fund

The Hotel Fund recorded a profit of € 20.7 million in 2016, compared with € 11.5 million in 2015. The Fund‘s total return rose to 14.2% in 2016 from 8.4% in 2015.

Highlights of the year include a turnkey purchase agreement (together with the Office Fund) for a 115-room extended-stay hotel in the Hourglass, a multifunctional building in Amsterdam’s Zuidas business district. This hotel is a turnkey project and the Fund has signed a 20-year fixed-rent lease with tenant Premier Suites. The Hourglass building is scheduled for completion in 2020. The Fund also signed a Head of Terms for extended-stay accommodation (82 rooms) in Amsterdam Houthavens in December 2016 with the consortium Boot&Co, together with a 25-year lease with tenant City ID Group. Completion of the hotel is expected in the fourth quarter of 2018. The Fund acquired the Stayokay Hotel Amsterdam (112-room hostel) and signed a 25-year lease with tenant Stayokay.

Healthcare Fund

The Healthcare Fund reported a net result of € 1.1 million in 2016, compared with € 1.9 million in 2015. The total fund return (ROE) came in at 4.9% in 2016, 2.4% above budget and 2.8% lower than in 2015 (7.7%). Returns will be below the long-term target in the coming years, as the Fund acquires new projects, which result in no rent and therefore no direct income (rent), as most of the properties acquired will be new-build complexes.

In 2016, the Fund’s property portfolio increased to € 46.9 million from € 24.1 million at year-end 2015. The Fund added one new asset to the portfolio, the Martha Flora complex in Haarlem (as of December). Construction work started on the Aliantus Oud-Seyst in Zeist in August, and the complex will be completed in the summer of 2017. In total, the Fund signed transactions worth € 46.6 million in 2016. At year-end 2016, the Healthcare Fund had a pipeline of € 55.5 million in assets under construction or redevelopment.

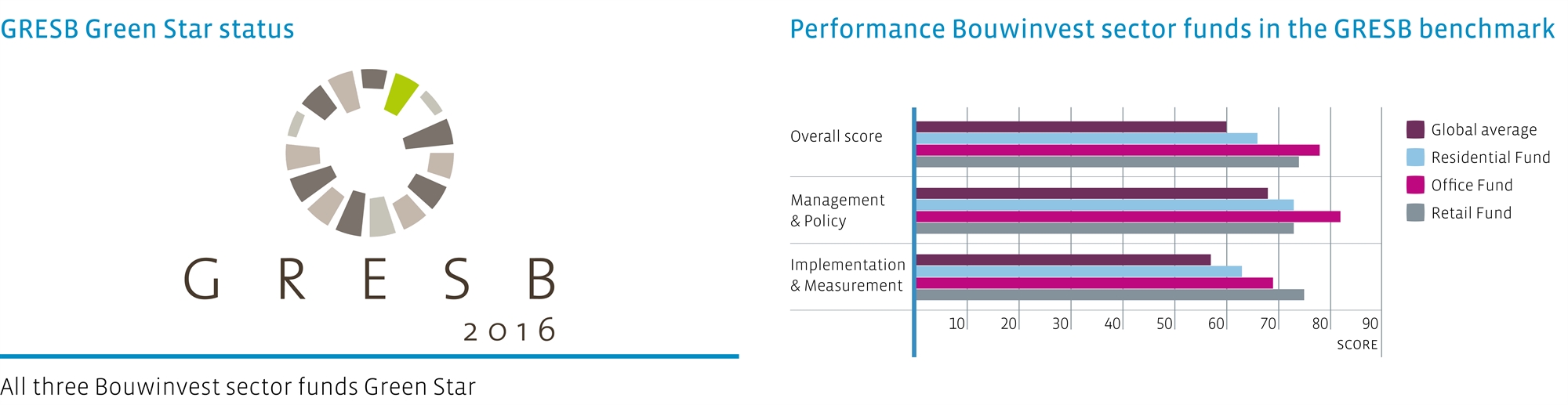

Dutch real estate funds retain Green Star status

Bouwinvest uses the Global Real Estate Sustainability Benchmark (GRESB) to measure and compare the sustainability performance of our three main Dutch sector funds. In 2016, Bouwinvest's three main Dutch sector funds once again actively participated in this initiative, which is aimed at boosting transparency and sustainability in the real estate sector. Thanks to this strategy and the actions that Bouwinvest continued to make last year, Bouwinvest's Residential, Retail and Office funds were awarded Green Star status for the third year in a row. Green Star is the highest possible category in the GRESB rankings and obviously we will be doing our utmost to retain this status in 2017 and beyond.